Ciro Rapacciuolo

Share on

The situation continues to deteriorate. Oil remains too expensive, because the truce in the Middle East has not reopened the Strait of Hormuz. As this shock drags on, its impact on economies is widening: inflation is rising in Italy too, household confidence is falling even further and the decline is spreading to business confidence, whilst the credit channel risks grinding to a halt. Consequently, consumer spending and services are at risk of slowing down, whilst the only driver for industrial production remains, for the time being, investment under the National Recovery and Resilience Plan (PNNR).

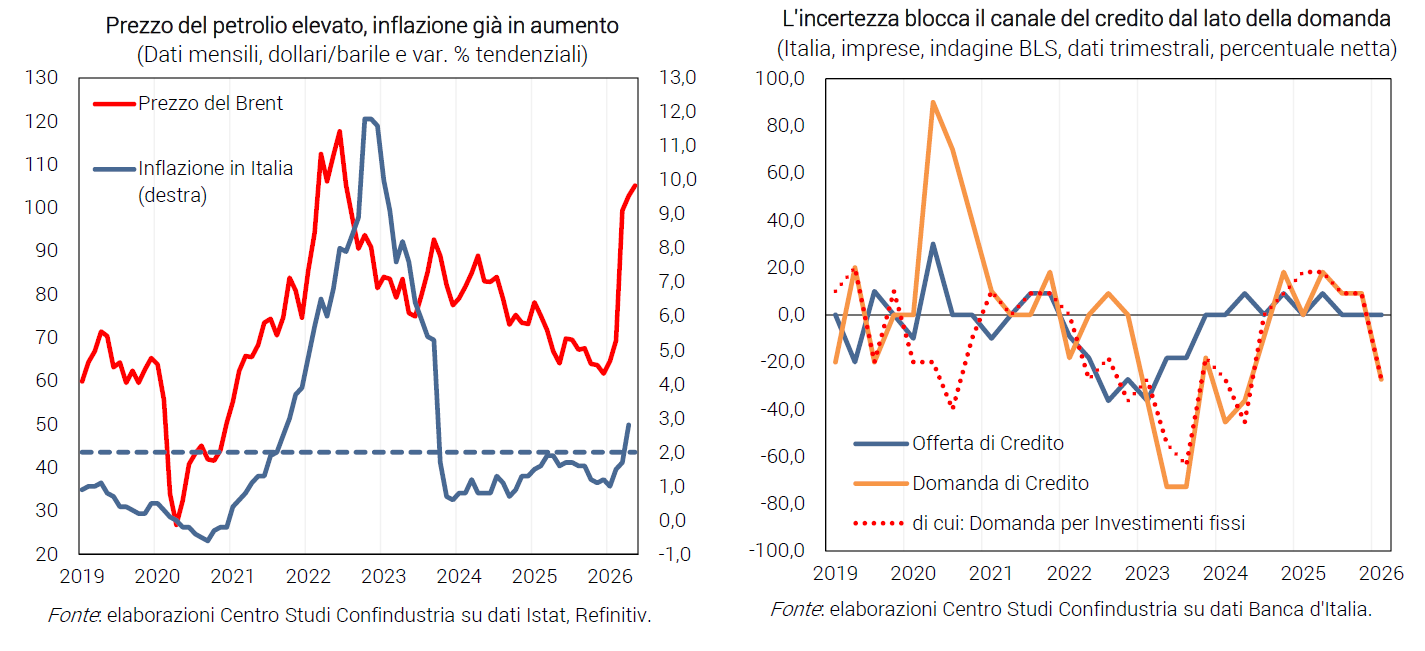

Oil prices remain high. The closure of the Strait, with shipping volumes still at record lows, is keeping the price of Brent crude high: $105 per barrel in May, just above April’s levels (103). It is confirmed that this war, unlike the one in Ukraine, is having less of an impact on gas prices, which in May (€46/MWh) remained below March’s peak (€53), but at levels well above those at the end of 2025 (€28).

Inflation is rising; interest rates are expected to rise. In Italy, the expected surge in consumer prices occurred in April (+2.7%, up from +1.5% in February), with energy prices already at +9.2% year-on-year, whilst core inflation has slowed so far (+1.7%). In Europe, inflation rose earlier and is higher (+3.0%, up from +1.9%), and even more so in the US (+3.8%, up from +2.4%). Whilst sovereign bond yields in Europe levelled off in May (in Italy at 3.81% and +79 basis points), the markets expect the ECB to begin raising its key interest rates in June (currently at 2.00%).

Investment: a slowdown is possible. Investment, including in non-residential buildings, is still being supported by the PNRR at the start of 2026. However, economic data point to a slowdown during the two months of the war: in the first quarter, demand for credit from businesses to finance investment fell, due to the adverse economic climate, and although the interest rate paid so far has not risen (3.38% in March); in April, confidence among firms producing capital goods fell even further.

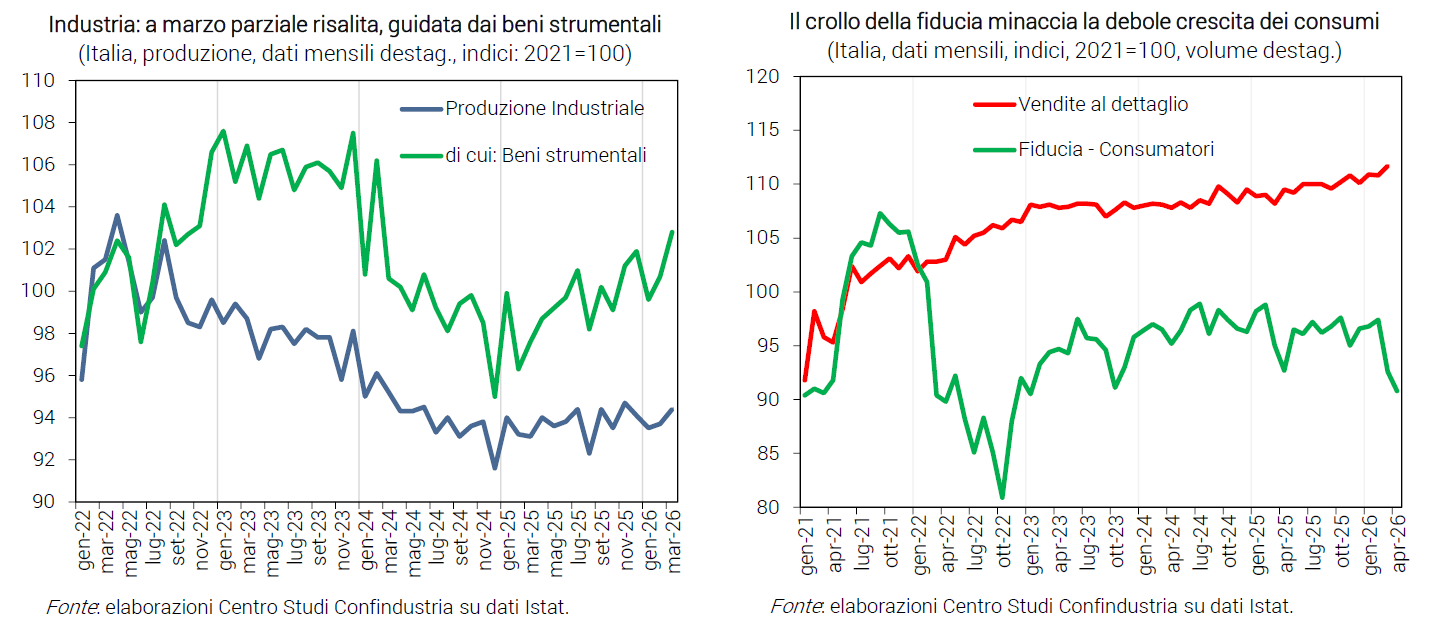

Confidence is falling, posing risks to consumer spending. In the first quarter, employment rose by +0.1%, providing little support for real income, which is under pressure from rising prices. In March, retail sales grew by 0.8%, with positive contributions from both food and non-food items; in April, car registrations remained buoyant. However, household confidence continued to fall, signalling an imminent slowdown in consumption, which is not being supported by a buffer of excess savings as it was in 2022.

The industry is holding up, but a downturn is on the horizon. In March, industrial production rebounded (+0.7%), driven by capital goods (+2.1%) – buoyed by the National Recovery and Resilience Plan (PNRR) – and intermediate goods (+0.3%), which firms are stockpiling as a precaution; this mitigated the decline in the first quarter to -0.2%. In April, however, the PMI signalled weaker demand, confirmed by a decline in firms’ assessments of orders, which has led to a deterioration in confidence, alongside a reduction in production expectations due to the unresolved war.

Services at risk of being suspended. The growth in spending by foreign tourists in Italy (+14% year-on-year in February) is at risk as the conflict in the Gulf continues. In April, the S&P Global Services PMI rose (to 49.8 from 48.8) but remains in recessionary territory, signalling weak demand; furthermore, business confidence in the services sector – which had held up in March – has fallen, with a particular decline in orders for tourism and transport.

Resilient export. In the first three months of 2026, Italian exports continued to grow (+4.0% in value compared with the fourth quarter of 2025); this was driven by increased sales both in non-EU countries (+4.8%) and in EU countries (+3.2%). In March, the first month of the conflict in Iran, sales growth consolidated, despite the slump in the Middle East (-52.5% year-on-year, down from +15.2%), which has so far been offset by strong growth in Switzerland (+84.6%), China (+23.9%) and the main EU countries.

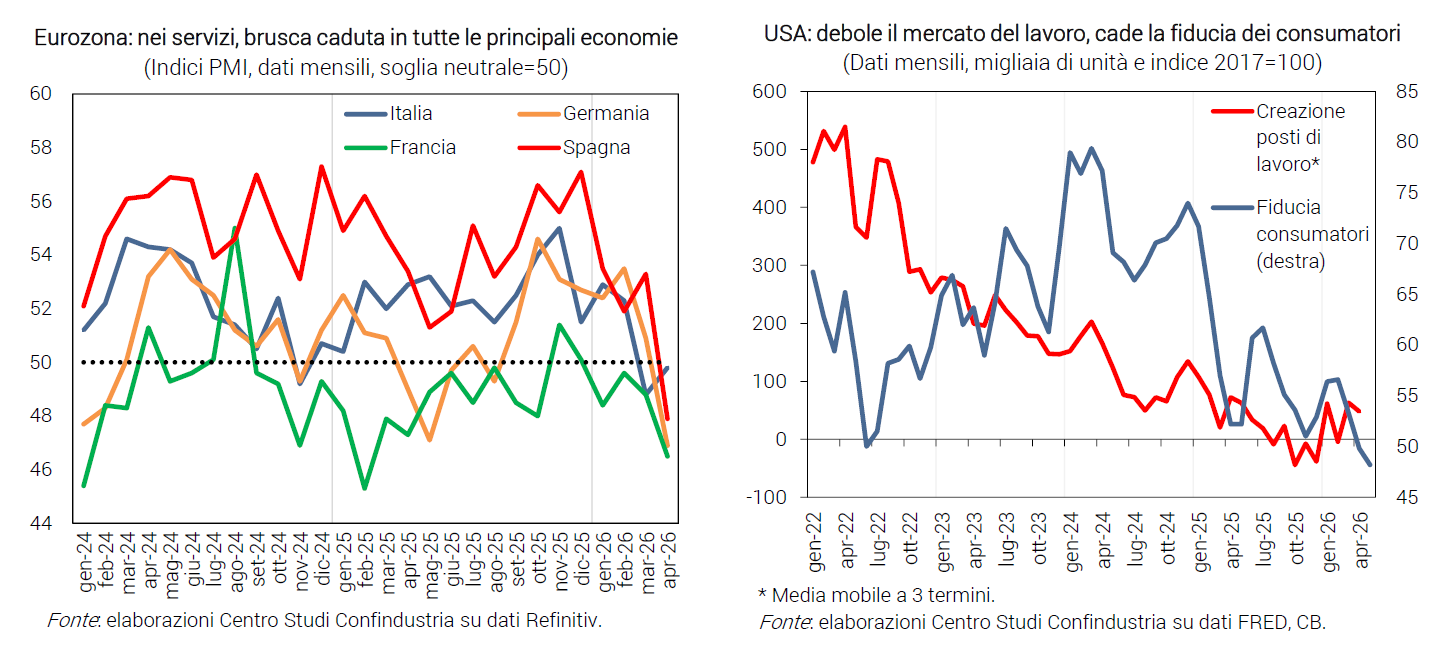

Eurozone: manufacturing is weak, services are struggling. In March, industrial production fell in Germany (-1.2%) and recovered in France and Spain (+1.0% and +2.4%); however, on average for the first quarter, the trends remained negative across the board. In April, the services PMIs all slipped into recessionary territory, whilst confidence and employment expectations fell sharply across the eurozone, and uncertainty continued to rise.

The US economy has weakened. Industrial production rose in April (+0.7%), at a slightly faster rate than in the first quarter (+0.5%); the Chicago Purchasing Managers’ Index, the PMI and the ISM provide mixed signals on the manufacturing sector: the first has plummeted, whilst the other two remain in expansionary territory. However, changes in employment figures and claims for unemployment benefits confirm the slowdown in the labour market which, together with the surge in inflation, has dampened consumer confidence in April–May.

China shows no signs of slowing down. In the first quarter, GDP grew by +5.0% year-on-year (+4.5% in the fourth quarter), despite tensions linked to the conflict with Iran. Industrial production accelerated to +6.1% over the quarter, driven by manufacturing and high-tech sectors. Signs in April remain positive: the manufacturing PMI rose to 52.2 (from 50.8), its highest level since the end of 2020, with production and new orders expanding. Growth is being driven primarily by exports, which recorded a year-on-year increase of +14.7% in the first quarter and maintained this pace in April, with a sharp recovery in sales to the US (+11.3%, up from -26.5% in March).

PNRR: crucial for growth, Italy among the best

Spending under the PNRR continues to increase. The Plan is at an advanced stage of financial implementation: the procedures initiated relate to 191 billion (98% of the total allocation of 194.4); financial commitments stand at 174.5 billion (90%), to which a further 12 billion – out of a total of 23.8 – is likely to be added, relating to measures included in financial instruments (so-called ‘facilities’) which have not yet been committed to date. Expenditure already incurred is slightly lower, amounting to 113.5 billion as of February 2026 (58%), of which approximately 9 billion has been spent since the start of the year; however, monitoring is hampered by persistent delays and discrepancies in data uploads to the REGIS platform. The CSC’s latest estimates projected expenditure of 35 billion for the whole of 2026: consequently, PNRR investments continue to be the main driver of GDP growth. Unused funds, or those arising from expenditure savings, will first be set aside in the State Treasury and then, after 30 June, may be reallocated to finance new initiatives or to refinance and reprogramme existing measures, in accordance with previously defined priorities.

2026: the most challenging phase of the PNRR’s implementation. This year will see the administrative closure of the Plan, the completion of the works still in progress, and the final reporting to the European Commission. Following the revisions made in 2025 and in the early months of 2026, the Plan has now entered its final phase, characterised by very tight deadlines and a significant increase in the pressure on public authorities and implementing bodies to deliver. By 31 August, the 159 milestones and targets linked to the tenth instalment (€28.4 billion) must be completed, whilst 30 September is the deadline for the formal submission of payment claims to the Commission.

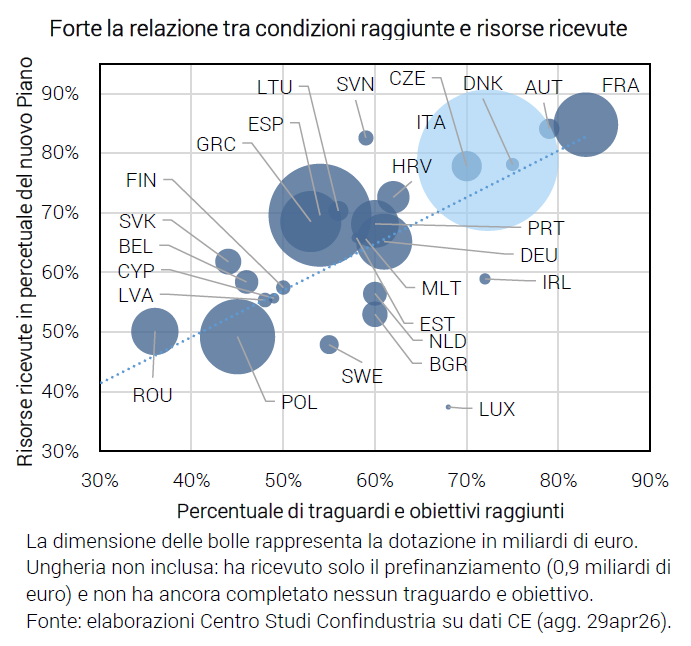

In formal terms, Italy is among the EU countries that have made the most progress. As at 29 April 2026, 416 out of 575 targets and objectives had been achieved, representing over 72% of the total planned, compared with an average of 50% for the other beneficiary countries of the EU programme (excluding the smallest ones). With the payment of the ninth instalment by May – currently in the final stages of approval – the funds received would rise to 166 billion euros, exceeding 85% of the Plan’s total allocation (compared with 53% for other European countries). However, the final phase of implementation appears more complex than the previous ones, as it mainly concerns infrastructure investments and projects characterised by longer implementation times and greater operational challenges.

The coming months will be crucial. The data available on the Italia Domani portal show that, in numerical terms, more than half of the projects have been formally completed; however, the majority of the Plan’s financial resources remain allocated to projects still under way. In fact, around 70% of the committed resources relate to projects that have not yet been completed, indicating that the success of the Plan’s final phase will depend above all on the ability to convert financial commitments into actual achievements by the European deadlines.

The European Commission has stepped up its monitoring during the construction phase. In recent months, there has been an increase in requests for preliminary checks on the progress of individual milestones and targets, with ongoing dialogue between EU institutions and national administrations. The aim is to avoid an excessive backlog of checks in the final phase of 2026 and to support the completion of the most complex measures.

The “substantive” assessment of the Plan remains pending. The first positive signs of a reduction in the time taken to implement projects and investments are beginning to emerge, thanks to the impact of the PNRR. The mechanism based on milestones and targets has, in fact, boosted implementation capacity. However, the tools for assessing actual outcomes and structural impacts on GDP, productivity, the quality of public services, and regional and social disparities remain weak. The final phase of the Plan will therefore be crucial in assessing whether the measures implemented are capable of producing lasting results in terms of economic growth, administrative efficiency and the reduction of disparities across the country.

Related

Join the largest business community in Italy.

Highlighted topics

Our Platform