Ciro Rapacciuolo

Share on

The economy stagnated in the second quarter. The agreement to end the war in Iran is shrouded in uncertainty, and ship traffic through the Strait of Hormuz remains limited. Whilst the price of oil has almost returned to pre-war levels, inflation remains high, interest rates have risen – which will curb lending – and foreign tourism has come to a sudden halt. The second quarter is expected to bear the brunt of the war’s impact, whilst the third quarter is set to show improvement. Industry has held up so far and investment is holding steady thanks to the PNNR.

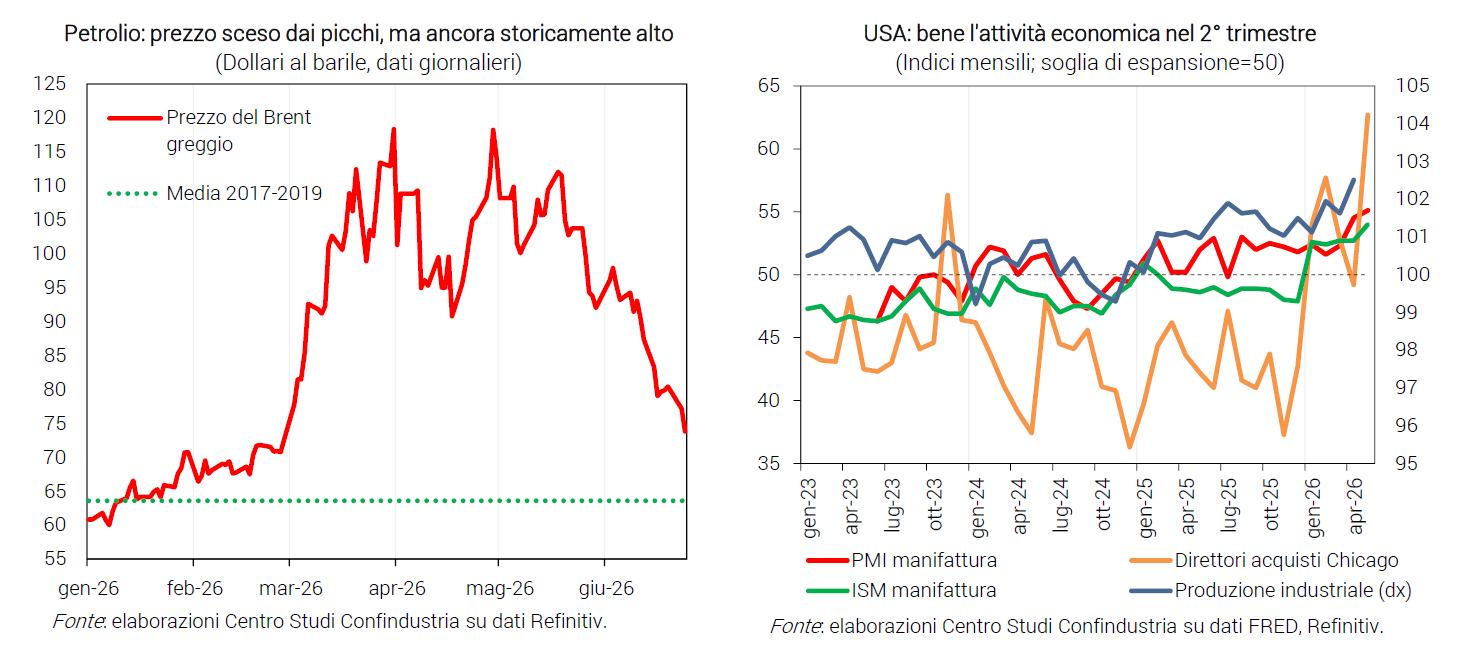

Oil prices are falling. Despite the US-Iran agreement, few oil tankers are currently passing through the Strait, and it will take months for the situation to return to normal. The price of Brent, however, has fallen in recent days (to $74 per barrel on 24 June), just above February’s average levels ($69), from a peak of $104 on average in May. The price of gas has fallen less sharply (€41/MWh on 24 June, with a monthly average of €45), remaining above February’s level (an average of €33) for the fourth consecutive month.

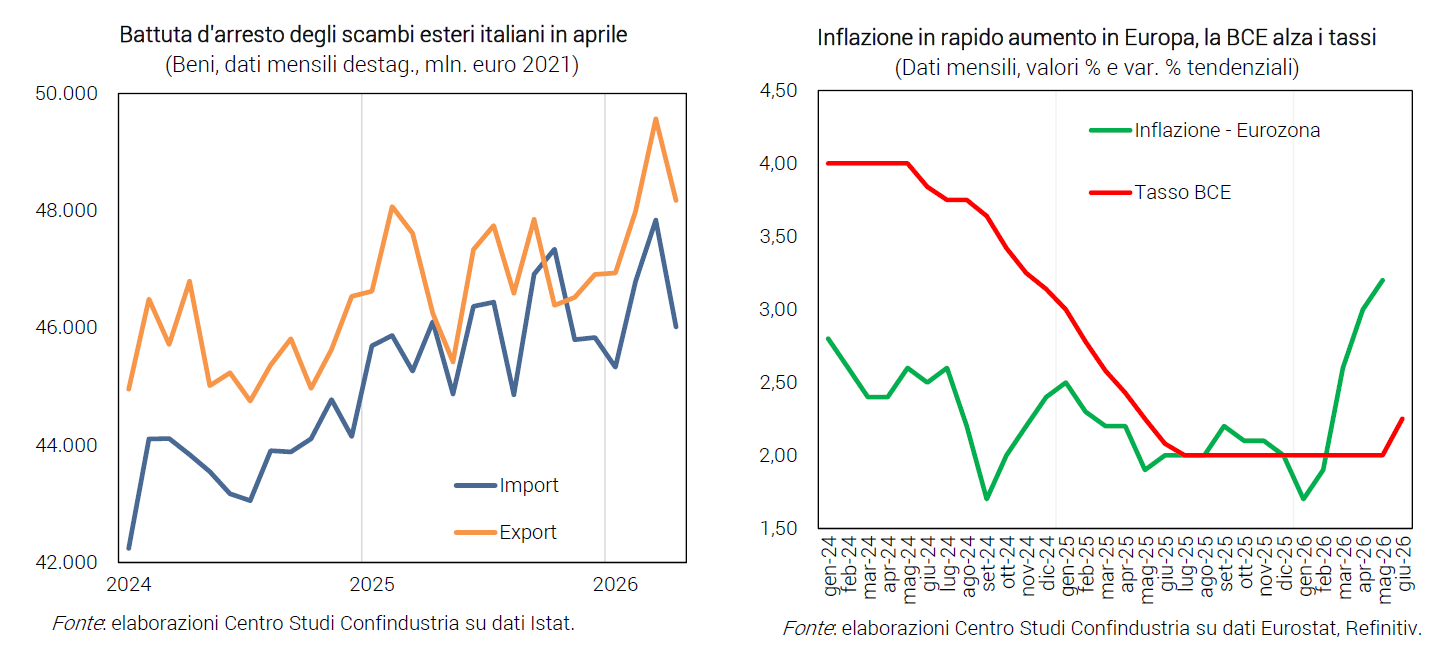

Inflation rises, interest rates go up. Driven by energy prices in May (+11.9% year-on-year), inflation in Italy rose to +3.2% (+1.0% in January), the same figure as in the Eurozone. Core prices have also started to rise again (+2.0% in Italy, up from +1.7% in April) and it will take time for them to ease. The ECB raised its key interest rates in mid-June (to 2.25% from 2.00%), but President Lagarde made it clear that this should not be seen as a significant tightening: the financial markets expect only a further +0.25 by the end of 2026.

Investments are becoming more difficult. Funding from the PNRR will continue to support investment for a few more quarters, but investment conditions have deteriorated and growth expectations have therefore been revised downwards: the rise in lending rates (average 3.56% in April) will curb the flow of finance, including for investment; furthermore, in June, confidence amongst capital goods firms rose only slightly and remains low.

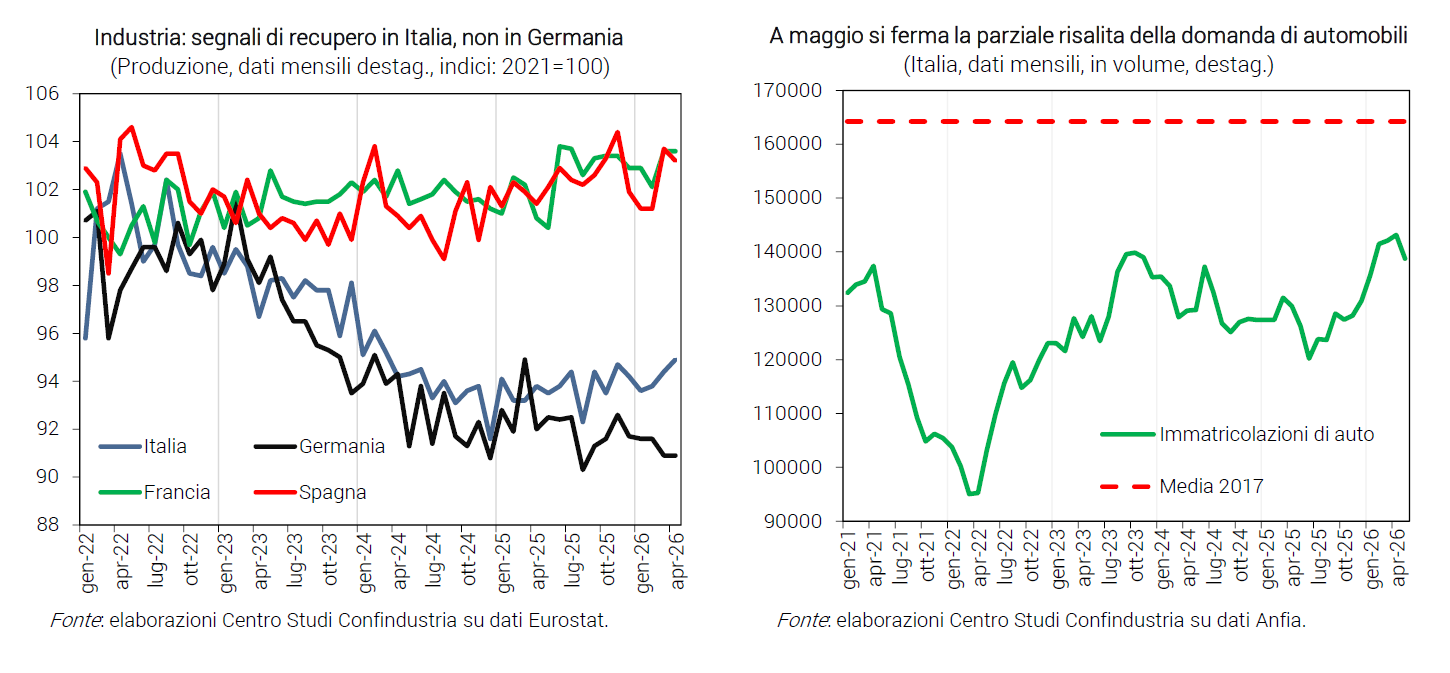

Consumption: signs of a slowdown. In April, employment continued to rise, supporting household incomes, which were, however, hit by rising prices. Retail sales fell by 0.3% in volume terms, for both food and non-food goods; and in May, car purchases were down, following the positive trend of recent months. This could signal a decline in consumption in the second quarter.

The industry is holding up. In April, industrial production rose by 0.5%, driven – as in the previous two months – by capital goods (+1.0%) and intermediate goods (+0.8%); growth in the second quarter stood at +1.0%. In May, the PMI strengthened into expansionary territory (52.9), signalling a slight improvement in demand, albeit supported by efforts to build up precautionary stocks of intermediate inputs. The international outlook (tariffs and trade war) remains the main source of uncertainty regarding the future.

Services not driven by tourism. The Gulf War, as feared, has brought the tourism boom to a halt: spending on travel by foreign visitors to Italy is now falling: -3.2% year-on-year in April, at current prices (down from +14.7% in February). The S&P Global PMI index confirms a moderate contraction in Italy’s services sector (49.4 in May), highlighting in particular cost pressures on businesses and a fall in demand. In June, business confidence in the services sector remained virtually unchanged, following the decline in April and May.

Exports: a setback. Italian exports of goods in April fell by 2.8% (imports fell by 3.8%, at constant prices), but the average over the last three months remains positive. The trends are very mixed: sales remain positive in the US, are improving in France and Germany, and are rising strongly in Switzerland and China; they are contracting in the Middle East, as well as in Turkey and Spain. By sector, metal products are leading the way and car sales are rebounding, whilst the pharmaceuticals sector is slowing and the textiles, clothing and furniture sectors remain weak.

Eurozone: German industry in decline. In April, industrial production fell in Spain (-0.5%) and remained stable in France and Germany, although the change recorded in the second quarter was -0.5% in both countries. In May, manufacturing PMIs were weakening in Germany, hovering around the neutral mark, and in France, just below it. In the services sector, France recorded the worst performance, with the PMI falling to 44.3.

The US economy is growing. Industrial production in May rose less than expected (+0.1%), but the trend in the second quarter is very positive (+1.0% realised). The manufacturing PMI, ISM and Chicago Purchasing Managers’ Index figures for May are all expansionary and on the rise. Growth in employment and low claims for unemployment benefits point to an improvement in the labour market, which tends to bolster consumer confidence, though this is being dampened by high inflation (+4.2%).

A two-speed China. In May, exports (+19.4% year-on-year) and industrial production (+4.5%) remained buoyant, driven by the automotive sector, semiconductors and high-tech industries; the manufacturing PMI fell to 51.8 (from 52.2), but remained in expansionary territory for the sixth consecutive month. Domestic demand, however, was weak, with retail sales down (-0.6%), the first decline since the end of 2022. On the price front, the gap is widening between subdued consumer inflation (CPI at +1.2%) and sharply rising producer prices (PPI at +3.9%, the highest since 2022).

Oil: risk of shortages not entirely ruled out; a critical summer lies ahead

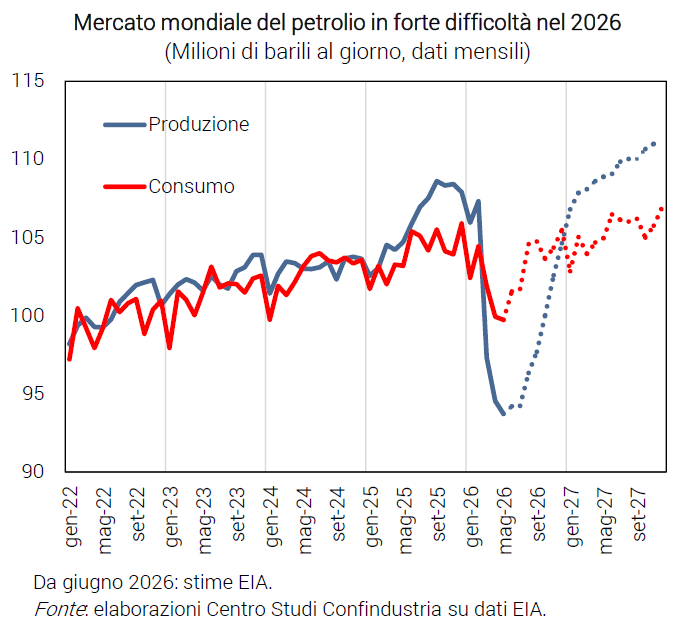

Production has plummeted. The data available for the period March–May 2026 show a sharp drop in global oil production (93.7 mbg, down from 107.3). This is all concentrated in the eight Gulf countries: the decline is greatest in Saudi Arabia and Iraq, and less so in Iran – which is a party to the war – with only Oman spared. The main reason is the prolonged restriction on transit through the Strait of Hormuz, combined with the physical limits on crude oil storage capacity in those countries: this has not only prevented around 20 mbg (pre-war figure) from leaving the Gulf, but has also forced the closure of many operational facilities. Damage to various oil infrastructure in the area has also contributed to this.

A slow and partial recovery. EIA estimates point to a slow and partial recovery in production in the Gulf (still -5.6 mbg by the end of 2026), even after a stable reopening of the Strait of Hormuz, which is expected to be completed in the third quarter: clearing the backlog of oil tankers takes time, and restoring damaged facilities takes even longer. By contrast, production outside the Gulf has not fallen and is expected to rise, particularly in 2027: the reason is the price elasticity of shale oil in the US, which is expected to grow significantly, driven by the high prices of recent months. This should help stabilise oil prices and justifies cautious optimism for Western economies, given that the surge in inflation in Europe and America is likely to remain largely temporary.

Supply will remain below demand for months. However, in the short to medium term, even with the Strait fully reopened, the expected trend in production will remain well below global demand. According to the scenario drawn up by the EIA, there will be as many as 10 months of sharp stock drawdowns (-5.2 mbg on average from March to December): a rare occurrence. This scenario also incorporates a contraction in global demand, caused by two factors: the rise in prices, which in 2026 will halt the decade-long trend of expanding oil consumption; and the restrictive measures adopted in Asia. This helps to narrow the gap between global supply and demand, but does not eliminate it.

Varying impacts. In such a scenario, there would be significant differences between the major regions. The US is a major oil producer and has recently become a net exporter of refined products (5.2 mbg), although it still imports a small net volume of crude oil (2.3 mbg); in the event of an international oil shortage, the impact on America would be moderate. Conversely, the EU – and even more so China and Japan – depend almost entirely on oil imports: before the war, a significant proportion of these came from the Gulf.

A comforting cushion. One very positive factor is that, prior to the conflict in the Middle East – particularly in 2025 – there had been a significant build-up of commercial oil stocks, as supply had long exceeded global demand: the shock came at the best possible time. Furthermore, Western countries have built up a significant level of strategic reserves over recent years, precisely to deal with situations such as the current one (1,406 mb in the EU). In the US, the EIA scenario forecasts a drawdown of commercial stocks and a massive draw on strategic reserves (1.0 mbg on average over 6 months), without any shortages.

Are further measures on consumption needed? The use of available stocks and the curb on consumption brought about by high prices should be sufficient to overcome the “U-shaped” trend in oil production, which is expected to remain low until the end of the year. The most critical moment will be the summer of 2026: everything will depend on how long transit through the Strait of Hormuz remains restricted. If the restrictions persist for a long time, there is a risk that restrictive measures will also be needed in the West to reduce consumption and avoid shortages.

Where the shortage would be felt most keenly. Should an oil shortage occur, certain economic activities would be directly affected. In Italy, the 2024 figures from the National Energy Balance Sheet show that crude oil and refined products are consumed primarily for freight transport and private cars and motorbikes (84.8%); the remainder is divided between industry (5.6%, particularly the petrochemical sector, which is already struggling), agriculture (4.8%) and domestic and office heating (4.6%); the proportion used for electricity generation is now minimal.

Related

Join the largest business community in Italy.

Highlighted topics

Our Platform