Ciro Rapacciuolo

Share on

It worsens the scenario at the beginning of 2026. In Italy, after a good Q4 2025 (+0.3% GDP) driven by PNRR investments, household confidence improved in January and services accelerated. Industry dynamics remain volatile and the recovery slow, penalised by the more depreciated dollar and still fragile consumption. The high and rising cost of energy may come down thanks to the regulations approved by the Government.

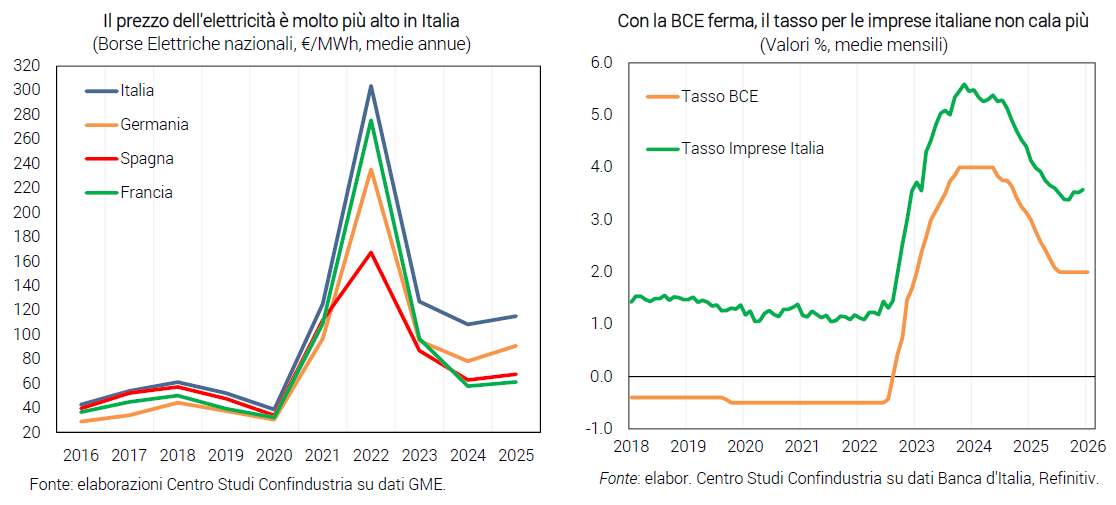

The “bills” decree is positive. The rise in the price of oil continues: 71 dollars per barrel in February (63 in December). After the flare-up in January, the price of gas remains at €33/MWh (from €28 at the end of 2025). The more depreciated dollar against the euro (1.18 in February), on the expectation of a FED more inclined to cut back, only partly mitigates price increases (and slows down exports). The decree passed by the government may reduce energy prices for households and businesses substantially, if approved by the European Commission.

The cost of credit goes up. In February, the rate on Italian BTPs fell slightly (3.36%), while the rise in the Bund in Germany stopped (2.97%): the spread narrowed again (+39 basis points, just +15 in Spain). The ECB, meanwhile, is stuck at a reference rate of 2.00% since mid-2025, even though inflation in the Eurozone has fallen to moderate levels (+1.7% in January). In this context, the rate paid by Italian companies has exhausted the decline and reversed course (3.58% in December, from 3.38% in September).

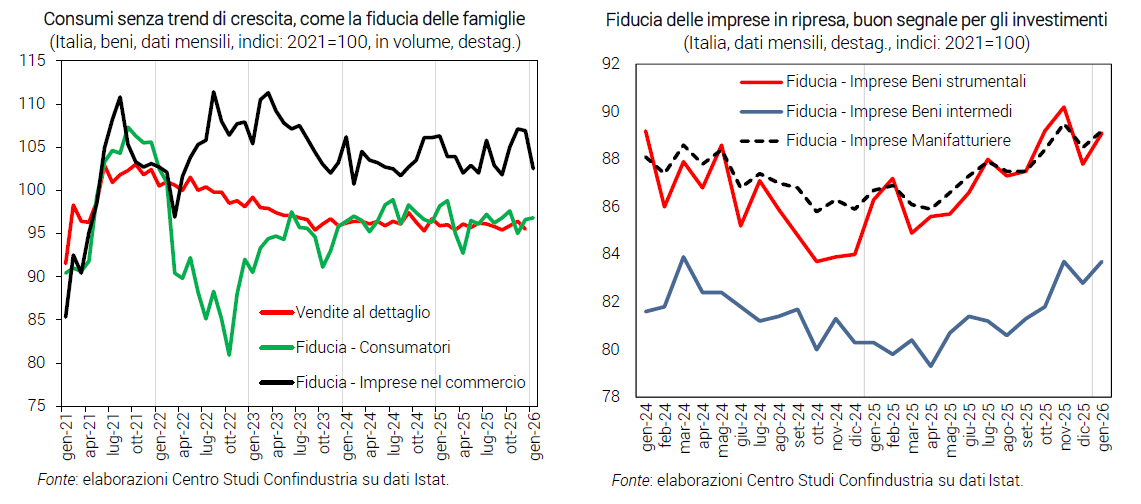

Investment: signs remain positive. Economic indicators show a favourable trend for investments in plant and machinery: in January, the confidence of manufacturing companies improved in total and, in particular, in the capital goods component. By contrast, the confidence of construction companies deteriorated for the third consecutive month, penalised by judgments on orders, although expectations on construction plans for the next three months were favourable.

Consumption: still slow start to the year. Retail sales fell in December (-0.9% in volume), almost cancelling out growth in Q4 (+0.1%); in January, however, car purchases increased. Household confidence improved somewhat at the beginning of 2026, while the number of employed persons, although contracting slightly at the end of 2025, still grew by +0.3% in Q4. Business confidence in trade, on the other hand, falls sharply, although sales judgments remain positive.

Services in acceleration. In December, the expenditure of foreign tourists grew slightly (+2.5% trend). In the first month of 2026, the HCOB-PMI, already in the expansionary zone, indicates a strengthening of the sector (52.9 from 51.5). Business confidence in services also rose robustly in January (103.4 from 100.2).

Industry: weak recovery. In December industrial production fell again (-0.4%, after +1.5%), but Q4 remained positive (+0.9%): there is an upturn, but a fragile one, because monthly data are very volatile and demand (from exports and consumption) remains weak. In January, the PMI improved slightly, remaining in the recessionary area (48.1 from 47.9), business confidence also rose slowly (89.2 from 88.5).

Volatile exports. Although Italian goods exports grew in December (+0.6%, at constant prices), they fell in Q4 (-1.9%). Imports expanded modestly (+0.1% monthly and +0.4% quarterly). Very heterogeneous dynamics between countries and sectors in 2025 show a rapid reconfiguration of trade after the shocks: exports were driven by pharmaceuticals to the US, metals to Switzerland; the pharmaceutical sector also generated much of the jump in imports from China and the US. The outlook for January 2026 remains weak according to foreign manufacturing orders, albeit slightly improving.

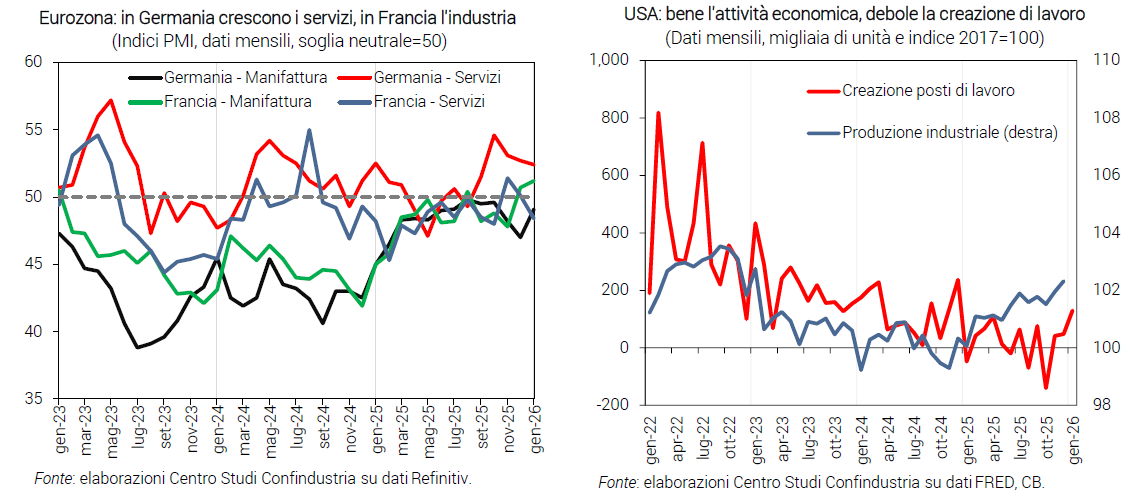

Eurozone: signs of a timid recovery. In Q4 the area's GDP grew by 0.3% and employment by 0.2%, with positive results in the main economies. In December, industrial production decreased a lot (-1.4%), but remained slightly up in Q4 (+0.3%). In January, PMI indices signalled an expansion only in services in Germany and in industry in France; confidence and employment expectations also improved across the area.

USA: good economy but weak jobs. Industrial production in December continued to grow (+0.4%), continuing the positive momentum since the beginning of 2025: Q4 ended at +0.2% and the PMI and ISM manufacturing indices confirm an expansionary profile in January 2026. Job creation also improved, but remains weak (+130K), after a Q4 2025 decline (-51K).

India: expanding manufacturing. In December, industrial production accelerated to an annual +7.8% (from +7.2%), above expectations; in January the PMI rose to 55.4 (from 55.0), signalling an improvement in orders, output and employment. On the trade front, the US-India agreement reduces US tariffs to 18% on average (from 50%), but doubts remain over rules of origin and India's commitment to $500 billion in purchases over 5 years, on goods that now total 23.

Industry: pharmaceuticals and metals good, cars and fashion bad

Still down, but something has changed. Italian industry, in aggregate, over the course of 2025 has slowly transitioned first to a “end of fall” phase, then towards the end of the year to that of a “partial and weak recovery”: we have not yet reached a clear trend reversal. On average for the year, moreover, the industry still recorded a new, albeit very small (-0.2%) reduction in output, following the large drop in 2023-2024 (-2.0% and -4.0%).

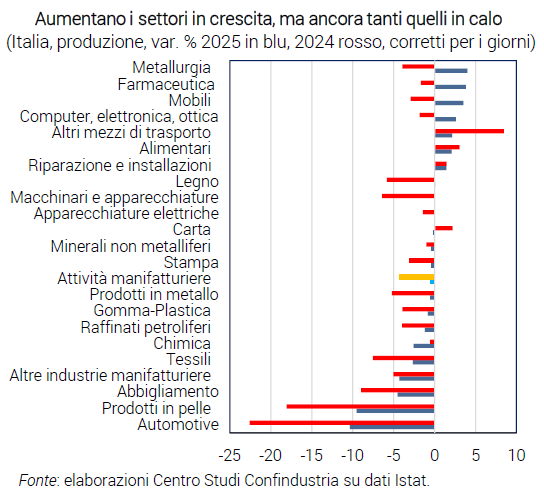

Various sectors are growing again. There are also indications of improvement at the sectoral level: the number of growth industries increased in 2025, compared to 2024: it rose to 9, from 4. This is because 6 sectors changed sign from negative to positive (including machinery, at a modest +0.04%) and only 1 from positive to negative (paper, at a moderate -0.1%).

But the road is long. However, only 3 manufacturing sectors (out of 22) grew in both 2024 and 2025, too few for robust aggregate dynamics. Conversely, as many as 12 sectors experienced declines in both years. The range of variation, at least, became less wide in 2025, from -10% to +4%, (compared to “-23%, +8%” in 2024), mainly because the largest declines in 2025 were smaller.

Automotive and “fashion” in trouble. These two sectors experienced two years of fall, although it eased in 2025. For the automotive sector (-10.3%), reasons include rising prices, uncertainty about regulations, and increased imports. Textile-clothing-leather (-5.5% in aggregate) is penalised by falling exports and still low household confidence, in an economy that is growing only slightly. Chemicals is the only one that, bucking the trend, shows a larger drop in 2025 (-2.6%) than in 2024: it is a sector with structural problems, because it is affected by expensive energy also used as a raw material, and registers plant closures and cases of conversion to new production (biorefineries, energy storage) throughout Europe.

Pharmaceuticals and metallurgy are relaunched. Pharmaceuticals, among the growth sectors (+3.8%), saw exports rise sharply: +28.5% year-on-year, the highest of all sectors, with an external surplus of EUR 11.4 billion, confirming a strong international specialisation; growth towards the USA (+54%), linked to stockpiling, stands out. The metal sector (+4.0%) was also moderately supported in 2025 by the export channel, despite the high duties imposed by the US (on steel and aluminium).

Food against the trend. The food sector grew in both years (+2.6% on average production in 2024-2025), among the few that did not fall, along with “other transport”, despite both slowing down in 2025. This confirms a historical characteristic of food, namely being an “anti-cyclical” sector, which does well in difficult economic times. Given its tonnage (15.2% of industry, as production sold), food gives vital support to the rest of the business in such periods.

Obstacle and push factors. There are transversal factors holding back all industrial sectors (albeit with different intensities), as well as the entire Italian economy: expensive energy; the weak dollar, tariffs, and therefore declining exports of goods; high uncertainty; high household savings and therefore sluggish consumption. On the other hand, lower interest rates compared to 2023, credit for companies that has started up again, the good investment dynamic (especially in machinery) that creates demand for various sectors help industry.

Better prospects for 2026. For the year just started, they are not yet available hard data from ISTAT sources, but only some economic indicators for the first month, which suggest a slight improvement. The dynamic that should prevail in 2026, for the Italian manufacturing aggregate, is one of moderate growth, thus returning to the positive sign after three negative years: this would actually be a partial recovery of the levels lost in recent years. In such a scenario, some sectors could stop losing production, while the number of sectors registering an increase could still rise. Not enough, in some cases, to heal recent losses, but at least the beginning of a positive path.

Related

Join the largest business community in Italy.

Highlighted topics

Our Platform