Ciro Rapacciuolo

Share on

Complicated scenario. The further announcements on US tariffs have raised uncertainty and eroded confidence: together with the devalued dollar, these are bad news for exports, consumption, investments. Positive news comes from the partial return of oil prices, contained inflation, the path of rate cuts in the Eurozone. Italian industry appears stagnant in the second quarter, while services are growing only slightly.

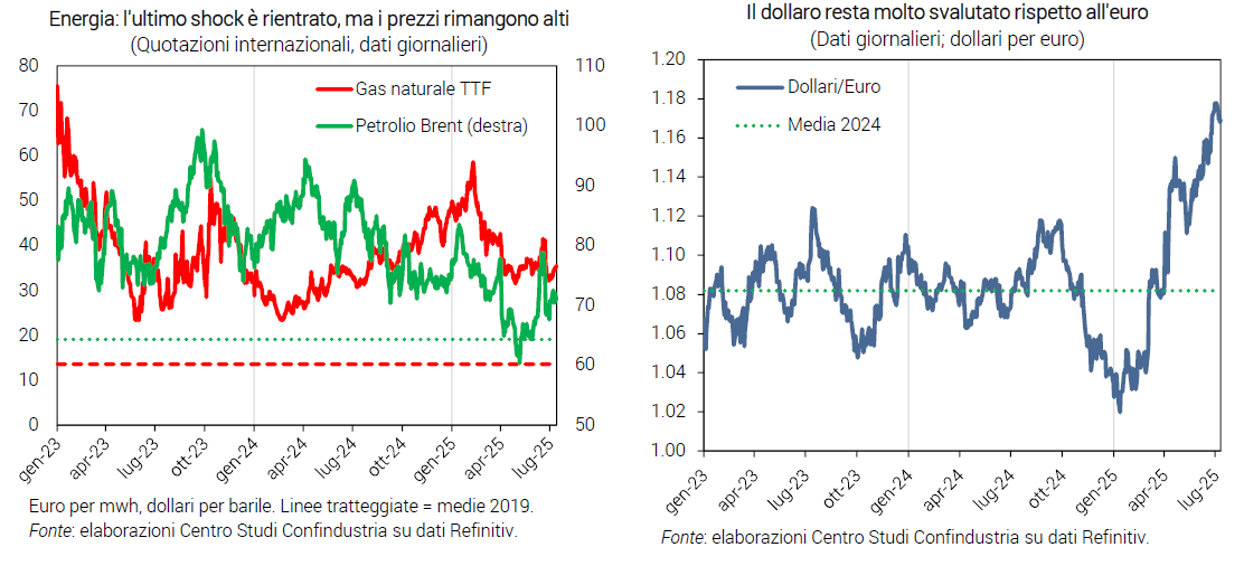

Dollar devalued. The dollar exchange rate remains heavily depreciated against the euro (little against other currencies): 1.17 on average in July with peaks at 1.18, from a low of 1.04 in January (+13.3%) and 1.08 on average in 2024. The weakening is fuelled by tariffs and worsening expectations on the US economy.

Energy Truce. The jump in oil prices in June proved short-lived, thanks to the ceasefire between Israel and Iran (71 1TP7/barrel on average in July, from a peak of 79 the month before). Quotations, however, remained high compared to the previous duty-related drop (64 USD on average in May).

Falling rates. Inflation remains low in Italy (+1.7% in June) and in the Eurozone as a whole (+2.0%). In three days' time, the ECB may cut rates again, raised to 2.00% in June. This lowers the cost of credit for Italian companies (3.7% in May) and continues to support the rise in loans (-1.4% per year).

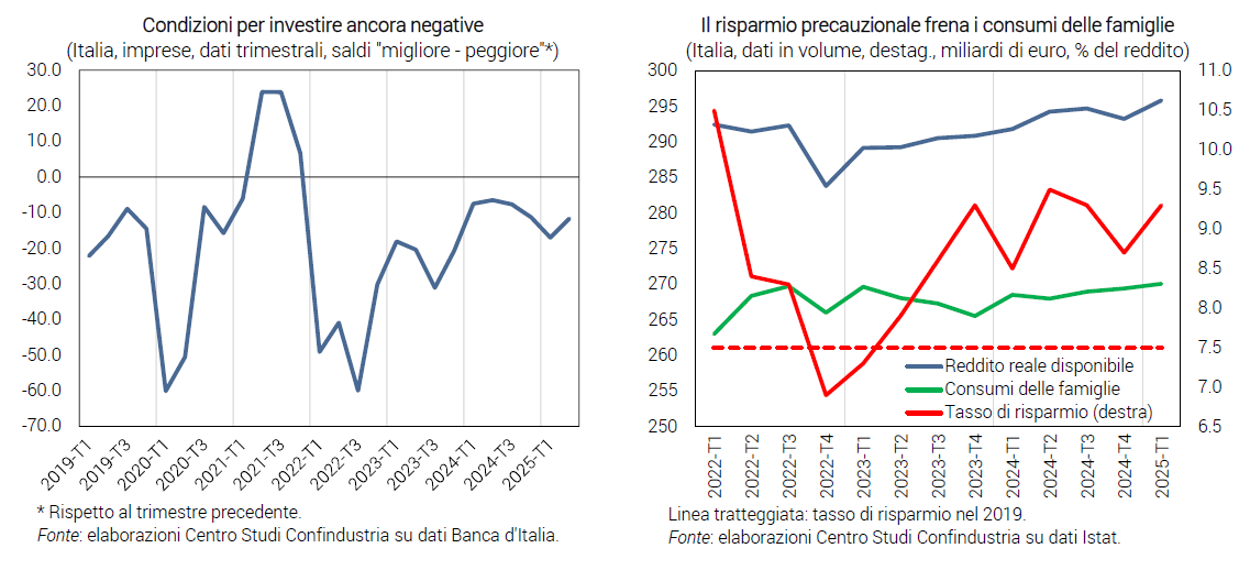

Weak investments. Indicators signalled a weakening in Q2: the conditions for investing worsened; business confidence recovered in June but at low levels (93.9 from 93.1 in May), down from Q1; orders for capital goods fell, negative for months (-19.0, from -17.7), although expectations turned positive. High uncertainty, the sworn enemy of investment decisions, weighed heavily.

Consumption under braking. In Q1 real income grew at a good pace (+0.9%), but consumption increased much less (+0.2%), held back by the increase in the savings ratio, due to uncertainty and low household confidence. For Q2 the scenario is not much better: employment grew slightly in May, but confidence fell again in June, retail sales recorded a zero change and car registrations plummeted (-17.4% per year).

Services slow down. For Q2, service indicators are somewhat less favourable. Spending by foreign tourists grew by +5.2% annually in April. RTT (CSC-TeamSystem) estimates a growing turnover in the quarter, despite a decline in May. The HCOB-PMI fell in June, although indicating expansion (52.1 from 53.2), while business confidence rose for the second month in a row.

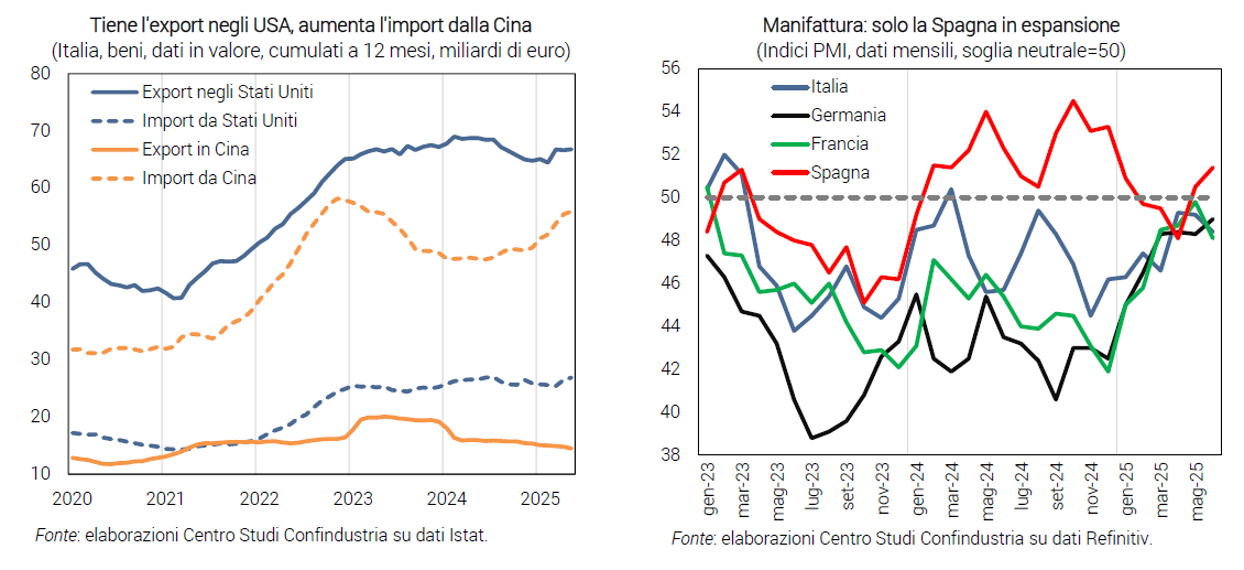

Industry falls again. In May, production fell again in Italy (-0.7%), after the good figures in April and Q1. RTT had anticipated May's decline in industry (in terms of turnover) and the CSC survey in June suggested caution among companies: duties put manufacturing at risk again. In June, the PMI fell further into recession (48.4 from 49.2), while industrial business confidence recovered for the second month, driven by expectations.

Exports already weak and at risk. Italian goods exports fell in Q2 (-3.6% in value in April-May compared to Q1), especially in non-EU markets (-5.7%), less so in intra-EU markets (-1.5%). The trade deficit with China widened: our exports fell, imports rose sharply. Trade with the United States is still holding up, but in a climate of great uncertainty (see Focus).

Eurozone in trouble. In May, production decreased in France (-0.5%), increased in Germany (+2.2%) and Spain (+0.6%). In June, however, indicators signalled declining confidence and high uncertainty. PMI indices for services and manufacturing suggest a struggling Eurozone in Q2 (in both sectors, Germany and France are struggling), with the exception of Spain expanding.

USA: production up. US GDP in Q1 was revised downwards, more than expected, although it was only marginally negative (-0.1%). In June, industrial production was higher than expected, in line with the manufacturing PMI (52.9 from 50): in Q2 it grew by +0.3%. Consumer confidence improved in July, also due to the strong increase in employment (+147 thousand).

Healthy China. GDP growth was +5.2% in Q2, driven by manufacturing (+6.8% year-on-year in June), especially high-tech sectors such as robotics and electric vehicles. Foreign demand remained robust (+5.8%), especially exports to South-East Asia (+16.8%) and the EU (+7.6%). Retail sales, on the other hand, slowed down (+4.8% in June, from +6.4%) signalling persistent volatility in consumption. The annual growth target at 5.0% remains uncertain and may require further stimulus to domestic demand.

US duties at 30% unsustainable: -0.8% impact on GDP

Changing scenario. The duties imposed on EU products at US customs, at 10% since 5 April, will rise to 30% from 1 August in the absence of an agreement between the parties. Higher duties are already in force on motor vehicles and components (25%), steel and aluminium (25% from March and 50% from June). The US duties could also be extended to goods currently exempt: pharmaceuticals, critical minerals, semiconductors, timber, aircraft and shipbuilding. EU countries would thus be among those most affected by the new US tariffs, on a par with China (increase of 30 points, from 21% to 51%). Many other countries are in fact subject to tariffs of 10%, while other major exporters to the US enjoy trade agreements limiting the size of tariffs (USMCA with Canada and Mexico, Economic Prosperity Deal with the UK).

High uncertainty and a weak dollar. Economic policy uncertainty in the United States has more than doubled under the Trump administration (+131% in the first half of July 2025 from December 2024 Economic Policy Uncertainty index), causing global uncertainty (+86%) to jump as well; both are at all-time highs, above the peak reached during the pandemic. Lower confidence about the prospects for the US, the leading global economy, fuelled a sharp depreciation of the dollar, especially against the euro (-13.7% since the beginning of the year).

Heterogeneous the first effects, negative the outlook. Italian sales in the USA held up in April-May (+0.4% trend), after accelerating in Q1 (+11.8%) in anticipation of the entry into force of duties (frontloading). The dynamics in the last two months diverged between sectors: those still exempt, but at risk of new tariff measures, such as pharmaceuticals (almost a quarter of total exports) and wood, grew strongly; those already subject to higher duties (metals and motor vehicles) fell; mixed results for sectors subject to duties at 10% (potentially tripled in August). According to a Bank of Italy survey, 80% of the companies whose main destination market is the US expect a reduction in exports from Q2 onwards. Of the total number of companies, 50% expect lower exports and 20% lower investments.

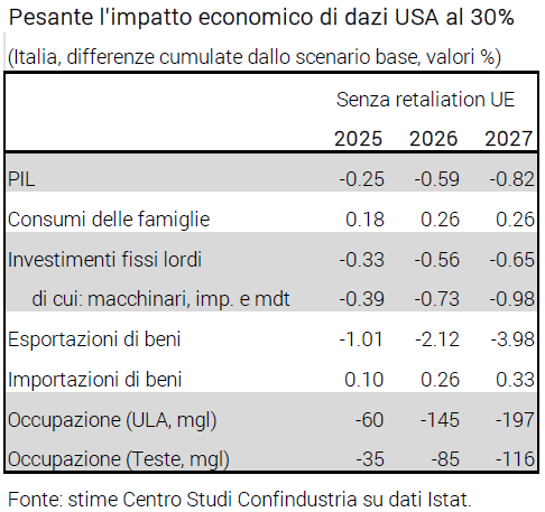

With duties at 30%, exports to the US more than halved. According to estimates by the Centro Studi Confindustria, with tariffs at 30% on all products and the euro-dollar exchange rate at current levels, Italian exports of goods to the USA would be reduced by approximately 38 billion, equal to 58% of sales in the USA, 6.0% of total exports and, also considering indirect connections, 4.0% of manufacturing production. The increase in duties and the devaluation of the dollar would reduce the price competitiveness of European exporters vis-à-vis both US domestic producers and those of other less affected countries. The impact would be amplified by uncertainty in transatlantic relations and the slowdown of the US economy. The estimated effect is medium to long term, i.e. in the case of permanent duties (and when parts of the processing in the US might be moved), because many high quality Italian products are hardly substitutable in the short term, especially in large quantities.

Strong net impact on GDP. The impact on our economy would be mitigated by the ability of Italian exporters to find new markets and compete on 'non-price' factors. According to a CSC simulation, sales of goods to the rest of the world would increase by about 13 billion cumulatively in 2027, offsetting part of the losses in the US market. However, total goods exports would fall by 4.0% and investments in machinery and equipment by 1.0%, compared to a baseline scenario without tariffs. Overall, the level of Italian GDP in 2027 would be 0.8% lower than in the path baseline.

Focus on domestic and other markets. In this context of constraints on the free international exchange of goods, it becomes crucial to strengthen the European single market, which is more resilient to global shocks, by reducing the internal barriers that still hinder the exchange of goods, services and capital (harmonisation of rules, strengthening of trans-European infrastructure, completion of the single capital market). It is crucial to encourage the geographical diversification of Italian trade, focusing on markets with high growth potential, such as Mercosur (destination of 7.5 billion Italian exports), India, Australia and the Asean countries.

Related

Join the largest business community in Italy.

Highlighted topics

Our Platform